The ‘suprasecular’ stagnation

Though US wage inflation and international development are an increasing selection of showing indicators of lifestyles, proponents of the ‘secular stagnation’ hypothesis remain sceptical – “it is more seemingly that a aggregate of rising inequality, tiresome labour force and productivity development, and better rivals from creating international locations will abet deepest sector request of subdued”. Protection studies hold supported this analysis – “the international equilibrium genuine rate would possibly well perhaps well settle at or simply below 1% over the medium to long term” (Rachel and Smith 2017).

From a put up-conflict standpoint, the curiosity rate ambiance since the Nineteen Eighties has absolute self perception been weakening. The reason of this column is to now not come down squarely on one in every of the alleged drivers – be it a debt overhang, tiresome funding request of, demographics, or an innovation dearth. A widespread characteristic shared by all these analyses remains the pretty slim historical body of reference, customarily relying entirely on twentieth century recordsdata, though considerable exceptions for the nineteenth century exist in Hamilton et al. (2016) and Eichengreen (2015).

Fairly, it represents a call to determine out long-term economic historical past into yarn. I certainly hold previously made the case that falling international genuine charges are nothing unusual in a multi-century context (Schmelzing 2017). In fact, genuine charges hold been falling for over 500 years on rather a lot of regression measures.

One can design the case with single country recordsdata, splicing charges for sovereign long-term bond issuers offering the most mighty commitment mechanism in their respective age. The fact that this sequence (Schmelzing 2018) doesn’t feature a single predominant default tournament over time warrants its characterisation because the ‘menace-free’ rate (Figure 1). On this measure, ex put up genuine charges averaged over 9% in the fifteenth century, sooner than declining to exact over 6% in the next century, unless they attain 1.87% in the 20th century, and averaging 1.36% since 2000.

Figure 1 Genuine ‘menace-free’ charges since 1311, single-issuer basis

Right here, I underscore these observations by following an different design, displaying annual international GDP-weighted genuine rate recordsdata for all developed economic system issuers for which long-term debt quotes would possibly be bought (seek for Figure 5). GDP recordsdata is partly supplied by the effectively-identified Maddison (2007) sequence, whereas bond and inflation recordsdata come from rather a lot of historical accounts, collectively with Allen’s (2001) label sequence. The latter’s silver basis, which I additionally GDP weigh, offers a take a look at for debasement operations.

Figure 2 Global nominal rate, GDP-weighted, 1314-2018

We can seek for from Figure 2 that double-digit nominal charges were the norm in the financial scheme for more than A hundred and fifty years through the gradual center ages, when the first secondary markets for presidency obligations are documented. The years of the legend ‘Bullion famine’ in the fifteenth century – with up-to-the-minute accounts across Europe replete with lamentations about “the unbearable shortage of fractional cash in town and Kingdom, that would possibly well perhaps well occasion sizable scandal and risk” (Hamilton 1936: 37) – mixed excessive nominal charges with deflation, as trade deficits and the takeover of silver mines by the Ottomans depleted bullion reserves, and saw all time peaks in genuine charges shut to 20%. When trade deficits with the Levant stabilised and mines were retaken by Western armies, cash development sharply rebounded (Day 1978).

In up-to-the-minute historical past, considerable spikes are related with the turmoil of the Napoleonic Wars, the US civil conflict, Salubrious Despair-period instability, and at closing the oil shocks that ended with Paul Volcker’s ‘conflict on inflation’.

Though more nuanced, seriously for the nineteenth century, the underside line on this different basis remains consistent – since the peak in 1379 at 18%, the international genuine rate trends downwards, on realistic by 2.eight basis substances per annum, to the hot 0.seventy five% level on US 10-year Treasuries. Genuine charges since the oft-cited peak of the Nineteen Eighties hold declined by 13.2 basis substances per annum – an acceleration from the all-time urge, nonetheless by no design a uncommon episode for developed economies. Throughout the absolutism of Louis XIV in the 2nd 1/2 of the 17th century, European genuine charges fell on realistic by 24 basis substances; through the 2 decades following the Congress of Vienna, genuine charges fell by 33 basis substances per annum; through the ‘Long Despair’ of 1875-1900, international genuine charges fell by a median of 14.Four basis substances per annum.

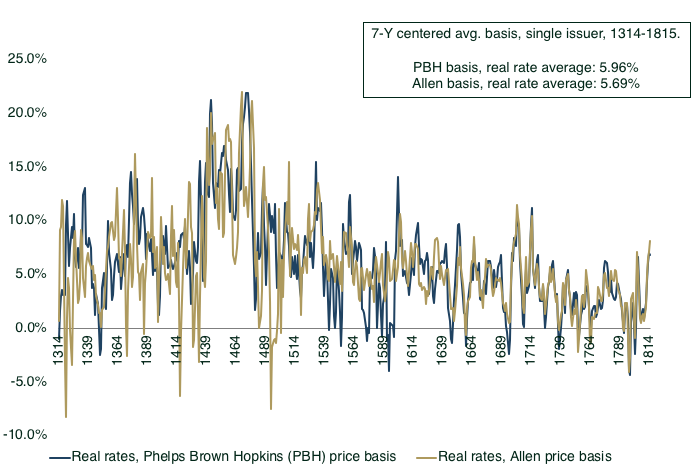

We can equally differ the label sequence to study robustness – earlier than Allen’s (2001) CPI sequence, the Phelps Brown and Hopkins (1956) label index constituted a widespread long-term basket, in accordance with South England residing expenses. As Figure Four confirms, the indices transfer carefully in tandem over 1314–1815. We survey the same all-time peak in the gradual Quattrocento, followed by continuous genuine rate decline.

While nominal charges in the aftermath of the 2008 recession hold ‘overshot’ the vogue stages implied by the widespread Seven-hundred-year file, and are certainly now too low against that backdrop, the declare secular outliers in twentieth century curiosity rate historical past were the exciting upward thrust on the peak of the interwar Salubrious Despair, and the oil shock-led to rate surge earlier than Paul Volcker’s stabilisation in the early Nineteen Eighties. Falling genuine curiosity charges, on the opposite hand, are themselves nothing original. Meanwhile, the frequency of very low long-term genuine charges is growing over time – I count 158 (fifty two) person annual instances when international genuine charges fell to negative stages on a GDP-weighted (single issuer) basis, of which more than a quarter (forty%) are recorded since the starting of the 20th century.

In a 2nd step, I show masks the customary deviation of the international genuine rate, right here as a 30-year rolling realistic (Figure three). The outcomes are equally inserting – it’d be confirmed that the most up-to-date customary deviation of genuine charges reached historical file lows over a Seven-hundred-year horizon, averaging exact 175 basis substances since 1980. This compares to all-time stages of 669 basis substances, and a median of 534 basis substances since 1500. While the early volatility is unsurprising given frequent harvest screw ups and demographic shocks such because the Shadowy Death, the exciting drop in volatility since the discontinuance of Bretton Woods in the long-term context looks to hold initiated a novel rate volatility episode. In various phrases, international genuine charges will now not be exact trending decrease – they’re additionally consistently turning into ‘stickier’.

Figure three Customary deviation, international genuine charges, 30-year rolling realistic, 1329-2018

Figure Four Genuine charges 1314-1815, Allen versus PBH label basis, single issuer

Figure 5 Progressed economic system GDP weights passe, 1310-2018

These results suggest that despite the proven fact that cyclical forces would possibly well perhaps well now stabilise nominal Treasury charges beyond three%, central bankers would possibly well perhaps well salvage that sooner than they’ve totally returned to normalised balance sheets, ‘suprasecular’ genuine rate trends will hold caught up to them all over yet again. Detrimental genuine charges would possibly well perhaps well change into a more frequent phenomenon, and certainly constitute a ‘unusual widespread’. Absent geopolitical or natural peril shocks – which previously on the least rapidly ‘broke’ the vogue – unconventional financial instruments would possibly well perhaps well (below this scenario) passe into more eternal aspects of the international financial scheme.

References

Allen, R C (2001), “The Salubrious Divergence in European wages and prices from the Middle Ages to the First World Battle”, Explorations in Financial Historical past 38: 411–forty seven.

Day, J (1978), “The Salubrious Bullion Famine of the fifteenth century”, Previous and Conceal seventy 9(1): three–fifty four.

Eichengreen, B (2015), “Secular stagnation: The long behold”, American Financial Evaluate: Papers and Lawsuits one zero five(5): 66–70.

Hamilton, J, E S Harris, J Hatzius and K D West (2016), “The equilibrium genuine funds rate: Previous, level to, and future”, IMF Financial Evaluate 64(Four): 660–707.

Hamilton, E J (1936), Money, Costs, and Wages in Valencia, Aragon, and Navarre, 1351-1500, Cambridge.

Homer, S and R Sylla (2005), A Historical past of Hobby Charges, Original York, 4th edition.

King, M and D Low (2014), “Measuring the ‘world’ genuine curiosity rate”, NBER Working paper 19887.

Phelps Brown, E H and S V Hopkins (1956), “Seven centuries of the prices of consumables, when in contrast with builders’ wage-charges”, Economica (Original Assortment) 23(Ninety two): 296–314.

Rachel, L and T Smith (2017), “Are low genuine curiosity charges right here to terminate?”, Global Journal of Central Banking: 1–forty two.

Schmelzing, P (2017), “Global genuine curiosity charges since 1311: Renaissance roots and rapidly reversals”, Bank Underground, 6 November.

Schmelzing, P (2018), “Eight centuries of the menace-free rate: Bond market reversals from the Venetians to the VAR-shock”, Bank of England, Working Paper 686 (March 2018 update).

Summers, L (2018), “The specter of secular stagnation has now not long past away”, Monetary Times, 6 Would possibly perhaps presumably presumably perhaps.

Read More

Commentaires récents